Download App

Better Online and Trade Show Sourcing Experiences.Scan the QR code to download.

Learn More

Hot Topics

by Vianie Li & Cecile de Veyra

LCD technology continues to hold its ground in the display market amid the emergence of next-generation OLED and MicroLED variants. The range of specifications it achieved over decades of development has helped it carve out a niche in many different applications, offering trade-offs that match market preferences.

Twisted nematic (TN) displays, the oldest liquid-crystal technology, remain a viable option if latency and price are the sole criteria. They have the best refresh rates and response times in the LCD sphere, although peers are catching up. Still, TN is the display of choice for budget desktops and laptops, including gaming units.

In-plane switching (IPS) screens offer the widest color gamut and viewing angle among LCDs. These, however, have what is called an “IPS glow,” which can be seen from an extreme angle or when viewing dark scenes in a dark room. Compared to TN displays, they typically have a slower response time.

VA screens are the middle ground, having better color reproduction than TN but none of the glow effect common with IPS. They also offer the highest contrast ratio. However, fast-paced transitions result in ghosting, blurring or smearing due to a slow response time.

In China, all three types are widely available. Manufacturers produce TN displays mainly for small and midsize mobile devices, VA displays for curved TVs and monitors, and IPS units for high-end TVs, monitors and portable electronics.

But in recent years, emphasis has been on VA and IPS LCDs. BOE, for instance, spent $1.77 billion to acquire CEC Panda’s 8.5G IPS and VA production line in Nanjing and 8.6G VA line in Chengdu in late 2020. In the same year, TCL/CSOT took over Samsung Electronics’ operations in Suzhou, which included an 8.5G fab and a co-located LCD module plant, according to Digital Supply Chain Consultants.

With the impending exit of Samsung Electronics and LG Display from the LCD market to concentrate on next-generation technologies, China was expected to wrestle the top spot from South Korea.

The two Korean companies, however, have put such plans announced in 2020 on hold amid a resurgence in demand. Samsung Electronics said it would continue to manufacture LCD panels until the end of 2022. "We'll keep going as long as we have customer needs," said an official at LG Display quoted in Nikkei Asia.

Even so, this has not dented China’s pursuit of LCD production expansion, driven by demand in TVs, monitors, laptops, tablets and smartphones.

About six high-generation fabs started mass production in 2020. CSOT’s 11G LCD+OLED TV fab line in Shenzhen and HKC’s 8.6G plant in Changshang, meanwhile, were scheduled to commence operations the following year. TCL/CSOT’s facility is expected to have an output of 89,000sqm every quarter and HKC’s 2.32 million sqm.

Small and midsize manufacturers will also continue to increase output by 5 to 10 percent in 2022, according to suppliers interviewed by Global Sources Electronic Components.

China-based Sigmaintell Consulting forecasts that BOE, TCL/CSOT and HKC will rank first, second and fifth in the global LCD panel category, with a combined share of 54 percent in 2022. As of 2021, BOE and TCL/CSOT had more than 50 percent share of the Chinese market, according to People’s Daily. The same source projects that China will account for 70 percent of the global capacity in the next three to five years.

“China-made panels are expected to dominate the market before OLED panel is mature enough to erode the market share of LCD panels,” according to Colley Hwang in Digitimes.

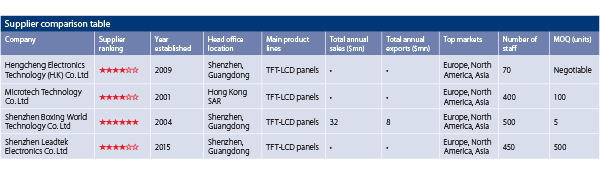

There are hundreds of manufacturers of LCD panels in China, mostly domestic enterprises operating on a small to medium scale in Shenzhen, Dongguan, Zhongshan, Hefei, Wuhan, Mianyang and Changshang.

Chinese suppliers offer small, midsize and large LCD panels for smartphones, notebook and tablet PCs, GPS devices, monitors and TVs.

They source key components and materials, such as polarizers, liquid crystals, substrates and film, from domestic or foreign providers, depending on buyers’ preferences.

LCD panel prices dropped in 2020 but rose steadily the following year driven by high input costs and demand domestically and abroad. Most Chinese suppliers adjusted their quotes by 10 to 20 percent. Prices may eventually stabilize, but manufacturers interviewed are not ruling out a fresh round of increases in 2022.

More Sourcing News

Read Also

关注 “环球资源外贸” 官方微信,获取实时外贸资讯

iOS & Android

iOS & Android(Mainland China)

Copyright © 2026 Publishers Representatives Limited. All rights reserved.